For twenty years, banks, index firms, and asset managers have tried to develop solutions to provide the diversification benefits of hedge funds with low fees and daily liquidity. This effort gained traction during the past decade as more and more institutional investors realized that, in a lower return environment, the traditional hedge fund fee structure could consume a disproportionate share of gross alpha. In this short note, we examine two potential solutions: factor modeling and alternative risk premia. The conclusion is that factor modeling has performed better than expected yet continues to face headwinds for widespread adoption among professional allocators. Alternative risk premia, by contrast, had great theoretical appeal and was quickly embraced by many allocators, yet has significantly underperformed expectations. The difference in outcomes sheds light on the nature of hedge fund returns, different conceptions of alpha, and structural biases among allocators.

Definitions

Factor modeling entails selecting a “target” – either a portfolio or index of hedge funds – and decomposing recent historical returns into the core drivers of performance across equity, rates, currency, and commodity markets. The thesis is that, for many hedge fund strategies, factor tilts explain most returns (including alpha) and portfolios shift slowly enough that the replication models can adapt in real-time. For non-quants, the argument is as follows: if you took a portfolio of, say, equity long/short funds and grouped every stock into the relevant market category (e.g. Large-Cap US, Small-Cap Value), then a portfolio of those “factor weights” via futures or ETFs should deliver similar performance over the near term.

Alternative risk premia products start with the assumption that most hedge fund alpha comes from specific trading strategies like merger arbitrage and currency carry. The thesis is that these strategies can be “replicated” using simple algorithms and delivered at a low cost. A typical portfolio will consist of a dozen or more trading strategies scaled to a specific level of risk.

Performance Objectives

Factor models seek to match or outperform the target portfolio or index. The concept is that an investor already is sold on hedge funds but wants a less expensive and more liquid version. If the target portfolio has a positive correlation to equities, so too will the replication; if hedge funds broadly decline, replication will as well. In this way, factor replication is “index-like.” A key innovation by some practitioners after 2008 was to pivot to target pre-fee returns: e.g. to deliver alpha through fee disintermediation, which potentially makes the products “index-plus.”

Alternative risk premia products generally target absolute returns with low or zero correlation to equities. A typical diversified product might target a 6% per annum net of fees with a 6% volatility or a Sharpe ratio of around 1.0. The theory is to extract a specific, valuable portion of hedge fund performance, not broadly replicate how hedge funds invest.

Divergent Views of Alpha

In the factor framework, hedge fund alpha comes primarily from factor tilts and exposure levels. Looked at this way, security selection leads to factor tilts that in turn deliver alpha. Examples include emerging markets equities in 2005-07 or tech stocks recently: the right category was more important than which stock a manager picked within it. This view of alpha is highly adaptive: as the world changes, talented hedge fund managers identify the best opportunities and pivot accordingly. The replication model simply holds on for the ride.

Alternative risk premia proponents believe that each trading strategy has a persistent and predictably high Sharpe ratio – perhaps 0.6 or 0.7, considerably more than traditional assets. Practitioners label these trading strategies “risk premia” under the theory that excess returns are available due to structural constraints (e.g. most investors cannot short) or heuristic biases. A diversified portfolio of such strategies, then, might achieve a Sharpe ratio of 1.0 or higher. With minimal equity beta, most returns will show up as a statistical alpha. In this model, hedge fund managers identified decades ago certain reliable, alpha-generating strategies and, today, risk premia practitioners can deliver the same at a low cost. This view of alpha is more static: what worked in the 1990s works today and will continue to work for the foreseeable future.

Performance: Back-test and Live

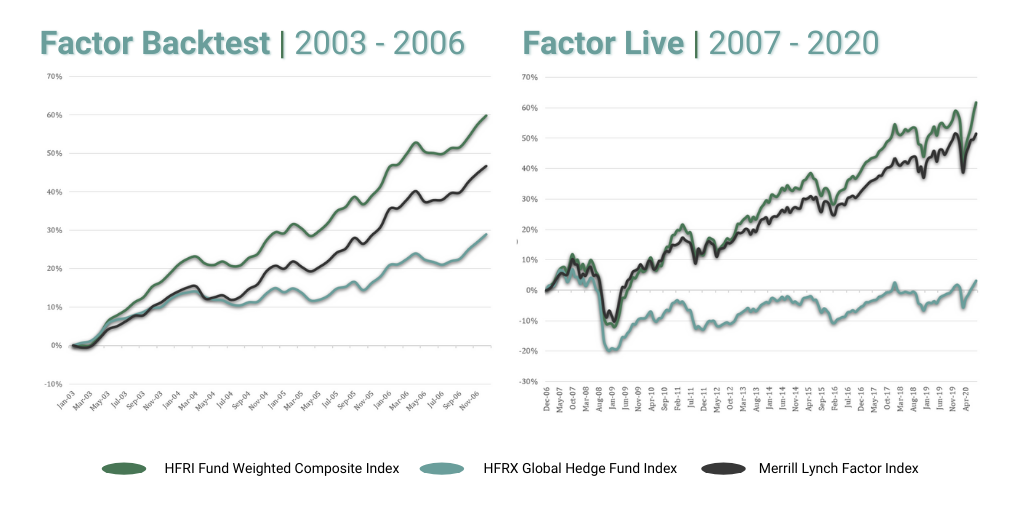

Factor models were introduced in 2006-07 with back-tested data as far back as the 1980s. The back-tested results showed that simple replication models – a dozen or fewer factors, rebalanced monthly – could closely match the performance of hedge fund indices. The Merrill Lynch Factor Index is a very good representation of the space: it seeks to deliver performance similar to the HFRI Fund Weighted Composite Index by investing in only six market factors, rebalanced monthly [1]. The charts below show the back-tested and live results compared to the HFRI Fund Weighted Composite Index and the HFRX Global Hedge Fund Index, which was built to solve the liquidity, if not the fee, issue with hedge funds. In both the back-tested and live periods, the replication closely tracks the returns of the (non-investable, illiquid) HFRI Fund Weighted Composite Index with a correlation of around 0.9 and materially outperforms the “liquid” hedge fund index.

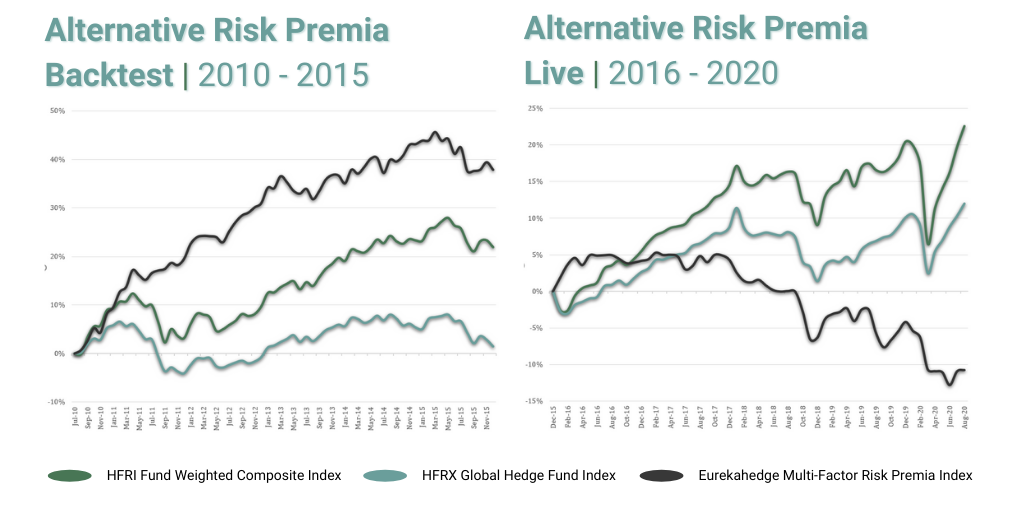

Alternative risk premia gained widespread traction later (2014 or 2015) when banks and asset managers launched a multitude of new products. Using the Eurekahedge Multi-Factor Risk Premia Index that was launched in December 2015, index data prior to launch provides a good estimate of back-tested results [2]. As shown in the below left, the back-tested figures aligned with (actually, exceeded) the theoretical return objectives: a Sharpe ratio of over 1.3 and much lower beta to equities than hedge fund indices. The live performance of the same index, however, shows the struggles faced by the space: while beta to equities has remained low, the index has a realized Sharpe ratio of -0.8 and a maximum drawdown of three times those in the hypothetical results.

Criticisms: Valid and Invalid

Right out of the gate in 2007, factor replication came under widespread criticism from hedge fund allocators and consultants. Lacking an empirical basis, criticism was grounded in the belief that it “should not work” given then-prevailing myths about hedge funds; few serious allocators would make the same arguments today. Similarly, allocators argued that replication only captured “average” performance, not the “best” funds; the counterarguments are that (a) the comparison is aspirational since there is little empirical evidence that one can select the “best” funds in advance, and (b) outperformance through fee dis-intermediation appears to be more reliable than manager selection. A more legitimate criticism in recent years has been that the models capture shifting exposures to various market betas, rather than more esoteric sources of return. This criticism has coincided with a shift in return expectations for hedge fund portfolios: from 0.3 or higher before 2008, to structurally lower beta targets and, often, in more illiquid strategies (e.g. structured credit).

The appeal of alternative risk premia was that it sought to address the criticisms above. The sources of alphas would be “orthogonal” and hence highly valuable in a diversified portfolio. When we closely analyzed the space in 2014, we struggled to connect the compelling theoretical arguments to real-world issues. First, the back-tested numbers were overstated, although we underestimated by how much. Second, the strategies were more akin to risky quantitative macro funds than merely “harvesting” risk premia. Finally, there was no compelling argument that these types of strategies should necessarily have high Sharpe ratios going forward since structural constraints diminish over time (e.g. shorting is hardly esoteric as it was in the early 1990s) as do investor biases when sound evidence is broadly disseminated. Over the past several years, practitioners have sought to argue that five years of poor performance should be viewed in the context of, to paraphrase, “seventy years of evidence that the strategies work”; however, since this defense also is based on theoretical results subject to the same biases as the back-tests above, it is hard to see how this position survives any rigorous scrutiny.

Conclusion

The performance success of factor replication has challenged several myths about (most) hedge funds: that hedge funds are nimble market timers, that individual security selection is more important than asset allocation, that investors on average are compensated for bearing illiquidity risk at the fund level, that alpha can overcome high fees. As institutional allocators came to recognize this, many shifted to more illiquid hedge fund strategies or those with structurally low equity beta Some of these strategies tend to charge higher fees (e.g. multi-strategy platforms) or stringent liquidity terms (e.g. structured credit), yet they are not conducive to factor replication. Rationally, allocators could replicate significant portions of their hedge fund portfolios and preserve fee budgets for those truly idiosyncratic strategies. Despite the empirical evidence, most professional hedge fund allocators still shy away from replication, arguably because its “index-like” nature is inconsistent with the “active” mandate to seek to identify funds that outperform.

Alternative risk premia products, by contrast, were built specifically to appeal to the professional hedge fund allocator who faced pressure to reduce fees. Like hedge fund selection, risk premia products are complicated and diverse and hence fit well into the ethos of hedge fund selection teams tasked with finding the “best” products. The marketing of back-tested results was brilliantly framed as “risk premia,” and hence built on the paradigm of investors used to speaking in terms of long-term market anomalies, like the value or momentum factors. One leading practitioner went so far as to ridicule allocators who did not invest, arguing that the strategies were as simple as picking low hanging fruits. That same practitioner’s flagship fund is down roughly 30% in the last three years – a probability of roughly one in 500,000 given its return and volatility targets. This is not an isolated event – every fund we track has materially underperformed the original lofty expectations. Confronted with a live performance that has no bearing to theoretical promise, there is a legitimate question about whether the entire space should be viewed as a failed experiment based on faulty assumptions.

About the Author

Andrew D. Beer has over twenty-five years of experience in the alternative investment business. For over a dozen years, Mr. Beer’s singular focus has been to identify strategies to match or outperform portfolios of leading hedge funds with low fees, daily liquidity and less downside risk. He serves as the Managing Member at Dynamic Beta Investments LLC (formerly branded Beachhead Capital Management) and is co-Portfolio Manager of the firm’s investment strategies.

Mr. Beer started in the hedge fund industry in 1994 when he joined the Baupost Group as one of six generalist portfolio managers working for Seth Klarman. During 1999-2004, Mr. Beer was the founding partner of three hedge fund firms in areas ranging from derivatives arbitrage to fundamental commodity investing to cross-border trading in Asia to quantitative methods of tracking actual portfolios.

Mr. Beer received his Master in Business Administration degree as a Baker Scholar from Harvard Business School, and his Bachelor of Arts degree, magna cum laude, from Harvard College. Mr. Beer lives in New York.

Footnotes

[1] We chose the Merrill Lynch Factor Index due to the simplicity of the model – six factors, twenty-four-month lookback, the target of HFRI Fund Weighted Composite Index – and the fact that the construction model has remained consistent since inception. Several other indices show similar results; however, some indices have additional complexity or shifts in construction methodology that render a long-term analysis less reliable.

[2] The Eurekahedge Multi-Factor Risk Premia Index is an index of bank-sponsored risk premia products. We selected this index because it is broadly representative of the category, rather than the performance of a single fund or product. There are two biases in the back-filled results. When a bank creates an index, the results prior to the launch date are subject to back-fill bias. Further, indices that underperform out of sample can be terminated with minimal disclosure, which can create a selection bias issue. We conducted our own extensive analysis of the bank products in 2014-16 and the pre-launch figures are consistent with what we observed.

The views expressed above are not necessarily the views of Thalēs Trading Solutions or any of its affiliates (collectively, “Thalēs”). The information presented above is only for informational and educational purposes and is not an offer to sell or the solicitation of an offer to buy any securities or other instruments. Additionally, the above information is not intended to provide, and should not be relied upon for investment, accounting, legal or tax advice. Thalēs makes no representations, express or implied, regarding the accuracy or completeness of this information, and the reader accepts all risks in relying on the above information for any purpose whatsoever.